Decoding Mortgage Insurance Premiums and Finance Charges

Table of Contents

Understanding Mortgage Insurance Premiums

Mortgage insurance premiums are a crucial, though sometimes perplexing, component of the mortgage equation, particularly for buyers who cannot make a substantial down payment. These premiums, which protect lenders in case of borrower default, can significantly impact the overall cost of a loan. In certain situations, mortgage insurance premiums may be classified as mortgage insurance finance charges, depending on the timing and method of payment. This is an important distinction that influences the loan’s annual percentage rate (APR) and total repayment cost. Mortgage insurance takes two main forms:

- Private Mortgage Insurance (PMI): Required for most conventional loans, PMI coverage enables lenders to assume more risk by accepting lower down payments. The cost of PMI is determined by factors such as the loan-to-value (LTV) ratio, the borrower’s credit score, and even the loan structure itself. Higher risk typically means higher PMI rates.

- FHA Mortgage Insurance: For mortgages backed by the Federal Housing Administration, mortgage insurance typically consists of both an upfront payment—usually paid at closing—and an ongoing monthly premium rolled into the regular mortgage payment. This structure is designed to maintain the solvency of government-backed lending while enabling broader access to homeownership.

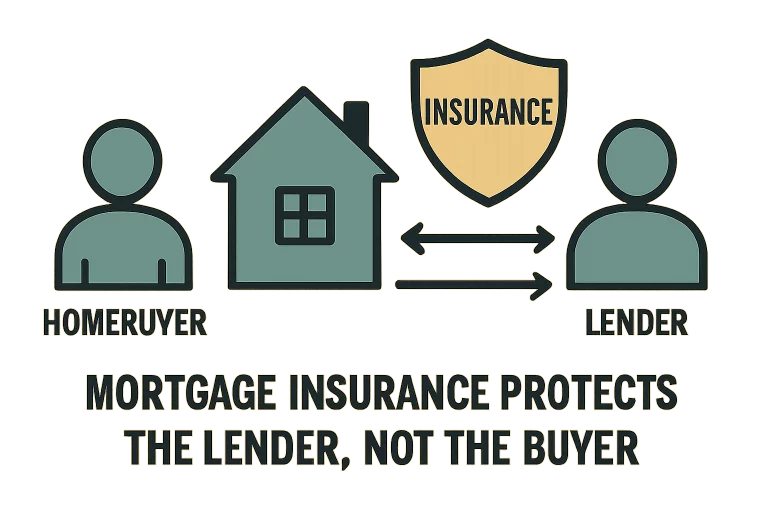

Both PMI and FHA mortgage insurance serve a single vital purpose: safeguarding the lender against financial losses if the borrower defaults on their loan. Although it might seem logical to assume that mortgage insurance protects the borrower, it is, in fact, strictly a lender safety net, ensuring lenders are reimbursed in the event of default. This distinction is crucial when budgeting and when comparing different loan options.

What Constitutes a Finance Charge?

The term “finance charge” has a precise, legally defined meaning, primarily established by the Truth in Lending Act (TILA). Its primary purpose is to create a transparent and standardized method for disclosing the true cost of borrowing over time, so that homebuyers have the information needed to make wise comparisons of different mortgage products. Finance charges generally include:

- All interest payments required over the life of the loan, from the very first to the last monthly payment

- Origination fees imposed by the lender for processing the loan application

- Other charges, such as discount points, certain forms of credit insurance, and various administrative fees tied directly to securing your loan

By requiring lenders to disclose the finance charge, TILA creates an equitable marketplace in which consumers can more easily identify the best deal for their unique circumstances. Borrowers should pay very close attention to this number, as it provides the foundation for calculating the Annual Percentage Rate (APR) and enables fair, apples-to-apples comparisons when shopping for a home loan.

Are MIPs Included in Finance Charges?

The question of whether mortgage insurance premiums are included in the finance charge is one of the most significant—and potentially confusing—issues facing homebuyers today. Federal law does not provide a universal answer; rather, the inclusion of MIPs depends on a combination of regulatory statutes, lender practices, the type of loan being issued, and the specifics of how and when the premiums are paid. According to regulatory distinctions, certain fees directly connected to mortgage insurance may or may not be counted toward the finance charge you see on your disclosures.

To clarify these distinctions, consider the Mortgage Choice Act of 2013—a landmark piece of legislation that amended the Truth in Lending Act. It ensured that, under certain circumstances, premiums paid into escrow for mortgage insurance are not included in the finance charge or considered “points and fees.” This clarification not only simplified the lending landscape for banks and mortgage companies but also offered greater transparency and relief to borrowers. The Consumer Financial Protection Bureau further outlines these rules in Regulation Z, specifically 12 CFR § 1026.32(a)(1)(ii)(A), which helps determine when mortgage insurance premiums must be included in the calculation of the finance charge.

Regulatory Perspectives

Regulatory oversight of mortgage lending has evolved in response to changing market conditions and a collective desire to protect consumers from hidden or excessive costs. The Mortgage Choice Act of 2013 played a crucial role in refining definitions and calculation rules within TILA, particularly as they pertain to mortgage insurance premiums, escrow deposits, and the disclosures provided to borrowers at closing. By clarifying how and when certain insurance-related fees are considered finance charges, regulators foster a more transparent and competitive lending environment, thereby reducing the risk of overcharging and enabling better decision-making.

Truth in Lending Act (TILA) Requirements

The overarching goal of TILA is to promote clear, honest lending through meticulous disclosure. It requires that all finance charges be itemized in a way that allows any consumer to see the actual cost of borrowing, not just the obvious principal and interest, but also select insurance, points, and administrative fees. Whether mortgage insurance premiums are included in the finance charge—or separated out as a distinct monthly or upfront cost—depends largely on how your loan is structured, when these premiums are assessed, and whether they are paid directly or via escrow.

Impact on Borrowers

The inclusion or exclusion of mortgage insurance premiums from the finance charge is not just a matter of regulatory paperwork; it carries practical implications for borrowers comparing loan estimates. The sum total of disclosed finance charges determines the loan’s Annual Percentage Rate (APR), which is the gold standard for comparing the relative cost of competing financial products. When MIPs are excluded from the finance charge, the APR may appear lower, giving buyers the impression of a better deal; however, the borrower remains fully responsible for paying these premiums as part of their monthly mortgage obligations.

This is especially important for buyers making smaller down payments, who are almost always required to pay some form of mortgage insurance. To get a true picture of the cost of homeownership, such borrowers should go beyond the disclosed finance charge and carefully calculate the long-run impact of insurance premiums on overall affordability, comparing not just the APR but also the total projected payments over the loan’s life.

Mastering the mortgage process begins with a full understanding of every charge, fee, and premium—whether it’s disclosed as part of your finance charge or listed as a separate line item. Here are several actionable strategies to help you take control:

- Review your loan estimate carefully. Focus on the finance charge and ensure that mortgage insurance premiums are either reflected in it or disclosed separately.

- Ask pointed questions about every charge, especially inquiring about which costs are due at closing and which will continue to be paid monthly. Knowledge is power—don’t hesitate to seek full transparency from your lender.

- If you’re unsure, reach out to a trusted mortgage professional or financial advisor. Their expertise can help you parse dense legal disclosures and project your full borrowing costs.

- Remain proactive and informed about current regulatory changes. Mortgage insurance requirements, premiums, and the manner in which they are disclosed can evolve due to new legislation or lender-specific policies.

In summary, a thorough understanding of the relationship between mortgage insurance premiums and finance charges empowers you to compare loan offers accurately, budget more effectively, and avoid unpleasant surprises, ultimately enabling you to choose the home and financing terms that best suit your goals. For more insights and detailed analysis of this topic, be sure to visit the primary resource on finance charges. The more informed you are, the better equipped you’ll be to chart a successful—and stress-free—path to homeownership.